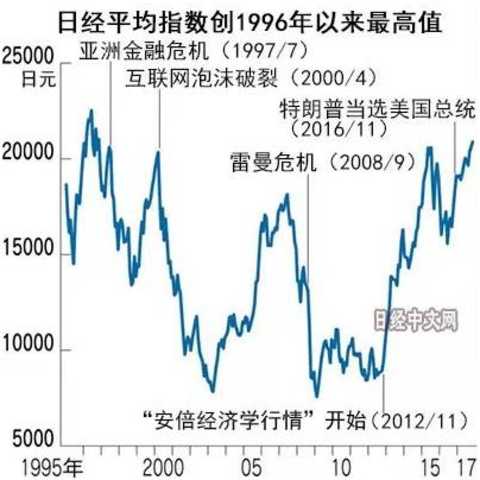

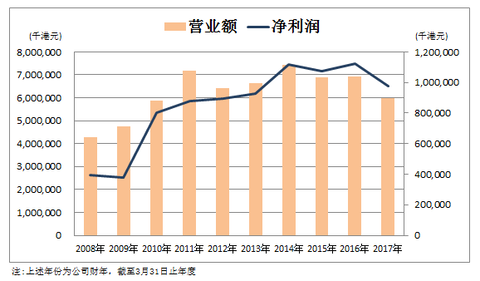

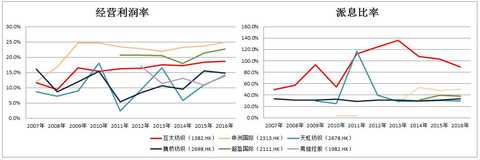

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction Client "Yunfeng has a fish cup" Hong Kong stocks simulation contest is hot, and the registration transaction is likely to win 600,000 prizes! [Click here to register] Source: Wang Yayuan Hong Kong Stock Exchange Text | Ellen When everyone is still predicting whether the Hang Seng Index can break through 30,000 points this year and challenge the new high in 2007, the Nikkei index of neighboring countries has quietly set a new high since December 1996 and nearly 21 years. The performance of the Nikkei Stock Index is partly due to the excellent performance of the recent month's share price of the global brand UNIQLO parent Fast Retailing. Last Thursday, the heavyweight weighted stock market value of 35 billion US dollars in fast-selling announced last year (September 2016 - August 2017) financial report: due to overseas UNIQLO business results, overall revenue during the period increased by 4.2% year-on-year to 18,619 For the billion yen, the profit attributable to shareholders rose 148.2% to reach 119.2 billion yen. Both revenue and profit reached record highs. On Friday, the share price of Fast Retailing rose 5.51%, and the fast-selling ADR (6288.HK) listed in Hong Kong also rose 8.8%, up more than 20% in the most recent month. Last Monday, our platform just published an article called <Article, which has risen 23% since last Friday. The market reaction is so enthusiastic. Apart from the company's valuation attraction and the good development space of the new business as mentioned in the article, I think another reason is also related to the fast-selling performance report. Half of the revenue of the old business of Nanxuan is from Xunxun. Sales, fast-selling future sales are optimistic, Nanxun's growth is more certain. Nanxuan Holdings> In addition to Nanxun, there is also a company in the Hong Kong stock market. Nearly half of the revenue is directly related to Uniqlo's sales. This is the relatively unlucky mutual textile (1382.HK). I. Vietnam plant suspended for nearly half a year I believe that there is no order for the factory. In addition, there is another thing that the boss can't avoid, that is, there are orders, but the factory is blocked and the workers can't work. The factory is shut down, and there are not only fixed expenses per month, but also compensation with customers. Mutual Textile has just experienced this difficult situation. The company announced in April 2017 that the factory entrance in Vietnam was blocked by the villagers and decided to suspend the operation of the plant until the incident was resolved. The incident stemmed from local villagers in Vietnam who were dissatisfied with the land compensation obtained by the government to recover its land for construction. After several months of negotiations, the company announced on September 25 that the Vietnamese government had cleared the blockage and the factory employees had been able to enter the plant. In recent years, Vietnam’s economy has taken off and prices have risen, largely due to the fact that more and more Chinese companies have begun to set up factories abroad. For the Vietnamese government, getting Chinese investment is a strong shot for economic growth. Therefore, Chinese investors have problems in Vietnam, that is, the economic blood system is directly hit, and the Vietnamese government will not solve it. Vietnam's plant capacity accounts for about 10% of the total production capacity of the company. Vietnam has stopped production. Although the company has transferred the affected orders to the factory in Panyu, Guangzhou, it will not be able to avoid additional expenses in the short term, such as delayed delivery of compensation. However, as the blockage is cleared, the company has made it clear that it will resume operations in November and the negative impact will stop. It’s like a rainy day, and there’s always a bad day, just as I believe the company’s performance will be better. Second, let the management be good, eat porridge or see customers First introduce the mutual textile, the company is a manufacturer and marketer of knitted fabrics. In addition to the previously affected Vietnamese factories (only 10% of total production), the company also has a major production base in Panyu, Guangzhou, accounting for 90% of total production. You may not have heard of the name of the mutual textile, but its customers will never be unfamiliar, except for the Uniqlo (Xunxing) mentioned above, as well as Victoria's Secret, Nike. US), An Dema (UA.US), and even the popular sports brand Anta (2020.HK). The company's revenue from Uniqlo and L Brands (LB.US) (including its brands including Wei Mi) is about 50% and 10% respectively. Although the company's customers are star-studded, its stock price has been a little bit sloppy on the ground since the second half of 2016. From the high of 11.08 yuan in 2016, the roller coaster fell to the current level of about 8 yuan. Recently, it has also hit a new low this year. Why is this? (Source: Futu Niu Niu) 1. High operational efficiency and stable dividend payout The performance of Mutual Textile has been for many years. From 2008 to now, the company's operating income and profit can be said to be stable and rising. The average compound annual growth rate of earnings is close to 11%, and the gross profit margin is also maintained at around 17%. (Source: Mutual Textiles Financial Report) During the fiscal year 2012~2014, the countries that benefited the end products of the company's products such as: the United States and other economic recovery and the impact of the growth of consumer confidence index, and the rapid expansion of the mutual textiles UNIQLO's UNIQLO in the world, the company's income and The increase in net profit is impressive. In addition, although revenues fell slightly in 2015 and 2016 after the peak revenue in 2014, the cost advantage of Vietnam was further reduced due to the cost reduction of Vietnam’s factory in Vietnam in the second half of 2015. In the case of a decrease in turnover, the company has brought a small increase in earnings. As can be seen from the chart below, the operating profit margin of the company has remained at around 17%, which is inferior to Hong Kong stocks, the leading Malaysian big brother Shenzhou International (2313.HK) and the company's high-end underwear materials. 2111.HK). (Source: 泓汇财ç») However, when it comes to the dividend payout ratio, Mutual Textile can be said to be a unique show and a leader. It has maintained a 100% level for many years. No peer can compare it. 2. Affected by weak customer demand Since its listing in 2007, Mutai Textile has not raised its capital record, and it has sent high interest rates every year. It has never paid a dividend of 5.89 Hong Kong dollars for ten years. Based on the company's initial listing price of 5.35 Hong Kong dollars, if you have not sold from the listing to the present, the dividend you received has exceeded your original investment cost, not to mention your hand value of 8 Hong Kong dollars per share. share price. However, in the 2016 and 2017 fiscal years, the company's revenue and profit both fell, due to the weak demand from customers such as Uniqlo and L Brands. In addition, the company is also a supplier to some US department stores (such as Wal-Mart, etc.). In 2016, the sales of US department stores were further eroded by e-commerce, which also led to a certain reduction in the orders of the company in North America. However, recently teammates began to notice that performance has clearly rebounded from the bottom. Third, the recovery of old customer demand, coupled with the addition of new customers 1. Uniqlo Let’s take a look at the recent performance of UNIQLO, the captain of half of the textile revenue of the company. As a well-known Japanese clothing brand, Uniqlo has opened nearly 500 stores in more than 100 cities since it entered the Chinese market in 2002. In 2017, Uniqlo plans to continue its rapid expansion, expanding the total number of stores worldwide to 3,336, including 100 new stores in China, the fastest-growing area in Uniqlo's global market. For the year ended August 31, 2017, Uniqlo's overall revenue increased by 4.2% year-on-year to 186.19 billion yen, while profit attributable to shareholders rose 148.2% to reach 119.2 billion yen. Revenue and profit reached record highs. The record is a good recovery performance. What about the 2018 fiscal year? Let's take a look at the outlook for the coming year in the company's 2017 report: (Source: Fast Retailing) Fast Retailing clearly stated that the overall revenue growth in FY18 was 10.1%, which is a significant increase from 4.2% in 2017. In the past one to two years, the Japanese market has been one of the main reasons for the overall slowdown of the company. From the table below, it can be seen that Japan’s growth in the second half of FY2017 has fallen sharply by 13.2%. (Source: Nanxuan Holdings) However, according to the just released Japanese sales data for September, Fast Retailing achieved a 6.3% same-store sales growth, reversing the downward trend in August due to reduced passenger flow. During the period, the number of customers increased by 3.9% year-on-year, and the unit price of passengers also rose by 2.3%, showing a rise for two consecutive months. Therefore, I believe that with the gradual recovery of fast-selling business in Japan, coupled with the strong momentum of overseas business expansion, it is absolutely possible for Fast Retail to achieve double-digit revenue growth in FY 2018! So it is not difficult to predict that the entire fast-selling supply chain income situation will usher in a big rebound next year. As one of the major suppliers of Fast Retailing, the company will have a great chance to receive more orders from Uniqlo. 2. Victoria's Secret In addition, let's take a look at the performance of the vice president of sexy underwear L Brands, who accounted for about 10% of the company's revenue, and was directly named in the company's financial statement for the fiscal year ending March 31, 2017. The reason for L Brands' sales decline in the first half of 2017 was mainly due to its main brand, Wei Mi. Wei Mi's swimwear series did not allow consumers to squander their pockets, which led to a drop in sales in the first half of the year. The same-store sales amount for more than a few months this year has fallen by more than 15%, which is quite exaggerated! In view of this, Wei Mi announced in August this year that it will no longer sell swimwear products and close the swimwear product line. As you can see from the chart below, sales of L Brands and Wei Mi began to pick up in July, and the downward trend seems to have slowed down. In August, data showed that the same store growth has narrowed to 4%, and the latest data in September is even further. It has risen to 2%, and some people in the market expect the data to achieve a positive growth recovery by the end of 2017. (Source: L Brands Monthly Sales Report) I think L Brands has a similar place with Fast Retailing, that is, both overseas market businesses have the opportunity to surprise investors next year. L Brands was previously cautious about the company's overseas expansion. As of March 2017, Wei Mi has 1,174 stores worldwide, and there are only 49 stores in overseas regions (nearly 96% of the market share in the United States), and it has not been timely allocated to the Chinese consumer market. Moreover, the retail stores of Wei Mi in the Chinese market were mostly authorized stores, and the store area was small. The only products that were sold were non-company products such as perfumes and accessories. L Brands management is clearly aware of this problem, not only from the beginning of 2016 to recover these Wei Mi "peripheral" storefront management rights, but also directly operated to obtain more profits, and Wei Mi also opened a new flagship store in Shanghai this year. Started to sell its core underwear products in China and began to eat the "big cake" in the Chinese market. According to statistics, the annual sales of the entire Chinese women's underwear market exceeds 100 billion yuan, with an average annual growth rate of nearly 20%. According to news reports, when the first flagship store of Wei Mi was put into trial operation in Shanghai, the scene was very hot. It can be seen that the Wei Mi brand is still very attractive to Chinese consumers. At the same time, the company also decided to hold a Victorian show with the theme of Chinese elements in Shanghai this year, which is the first time Wei Mi held a conference in Asia. The annual sales of the entire Chinese underwear market exceeds 100 billion yuan, with an average annual growth rate of nearly 20%. It can be expected that the adjustment of Wei Mi's global sales strategy and the positive expansion in the Asia-Pacific market will also drive the rebound of L Brands sales. And L Brands recently launched a new $250 million stock repurchase program, which also shows management's confidence in its future performance. 3. Other new brands In addition to the improved status of the existing teammates, Mutai Textile also received new orders from brands such as Under Armour, Calvin Klein and Anta in 2017. It is expected that orders from these brands will become new to each other. Source of income. Special mention here is Anta Sports. As a new leader in domestic sporting goods, Anta’s overall sales have increased by 19.2% from the data released in the first half of the year. Its stock price has risen by about 40% since 2017, which is better than the average performance of the industry. (Source: ANTA Sports) The customers of Mutai Textile have always been based on international brands. For the first time, domestic heavyweight customers have appeared, reflecting the upgrade of domestic sports brand products. The cost of materials or design has been able to catch up with international brands. Therefore, it is not excluded that the future customer portfolio of the company will become more and more domestic brands. 4. A 90-year-old Japanese listed company becomes a major shareholder On June 30 this year, the company ushered in a new transformation. Ye Bingyu, one of the founders and a major shareholder, sold all the shares of the company he held to Toray Industries (Toray Industries, Ltd., referred to as Toray, 3402.JP) at a price of HK$10 per share (approximately 11% premium). HK$4.05 billion. At present, Toray has become a major shareholder of the company, holding approximately 28.03% of the shares. Toray was founded in 1926 and listed in Japan in 1949. The current market value is about 1.8 trillion yen (about RMB 106 billion). Half of the company's revenue comes from the main business processing and sales of fibers and fabrics, in addition to plastics and chemicals, IT filling products, environmental and engineering services. As of March 30, 2017, Toray's revenue and net profit attributable to shareholders were 2,026.8 billion yen (about 111.9 billion yuan) and 99.4 billion yen (about 5.9 billion yuan). It is worth mentioning that Toray has had the same dividends as the mutual textiles in the past 10 years. It is believed that the dividend payout tradition of the mutual textiles will continue. (Source: Dongli official website) Toray has been a strategic partner of many internationally renowned retailers, including Uniqlo, which has been cooperating since 2006. The HEATTECH series of products is the result of the joint development of the two. Mutual Textiles has been a customer of Toray for 16 years, and purchases from Toray accounted for approximately 4% of the total cost of sales in FY2017 or HK$193 million. The founder of Mutual Textiles has three other founders in addition to Ye Bingyan, the original major shareholder who has sold shares. As can be seen from the above shareholding, there are two founders who no longer hold the company's equity, and the chairman and chief executive officer, Mr. Yin Huilai, holds less than 1% of the shares. At present, Zeng Jingbo, who holds the most shares, seems to be gradually reducing his holdings. On July 1, 2017, he was transferred to the non-executive director by the vice chairman. Toray also appointed his staff, Ishii Junshi, as an executive director, and became effective on October 1, 2017. (Source: Mutual Textile Company Announcement) In addition to the founders, according to the company's FY2017 annual report, Vice Chairman Liu Yaozhen and Lin Rongde, who resigned as a non-executive director on May 22, 2017, held 3.63% and 8.00% of the company's shares, respectively. However, from the current situation, the remaining founders should gradually withdraw from the mutual textile, Yin Huilai, who holds less than 1% of the shares, still serves as chairman and chief executive and believes that it is only a transitional arrangement. The garment manufacturing industry is a very traditional industry. In the middle of the manufacturing process, apart from strengthening automation, there is actually no innovation. What has always led innovation is in the use of materials, such as: some sports breathable fabrics in recent years or the HEATTECH series of Uniqlo. Toray is one of the leaders in global material innovation. Therefore, it is expected that Dongli will gradually take over the textiles in the future. It is expected to bring the effect of vertical integration in the long run, so that the company can know the trend of the clothing industry one step earlier than other peers. Help the company get a better order price. V. Conclusion The shutdowns and claims caused by the blockage of the Vietnamese factory will inevitably have a negative impact on the financial situation of the company. However, as long as we look at the stock price performance, we know that the market is fully aware of this negative news, and these are short-lived. The impact is not sustained, so the focus of the analysis should be on the future needs of the customer. Among the existing customers of the company, Uniqlo's business performance has significantly improved significantly. The overall revenue will have double-digit growth next year. The sales of L Brands as a drag bottle are also expected to pick up, plus new customers Under Armour, Calvin Klein. With Anta’s orders, Mutai Textile’s revenue in the coming year is recovering from the bottom. Based on the market average forecast, the current P/E ratios of the company's fiscal year 2018 (as of March 31, 2018) and fiscal year 2019 (as of March 31, 2019) are approximately 13 times and 11 times, respectively. In the past, the average price-to-earnings ratio of the company was 14 times. If it is analyzed in the fiscal year of 2018, the current price is only slightly underestimated. But the fact is that if you don't consider the unnecessary spending of nearly 130 million Hong Kong dollars in 2018 in Vietnam, the price-earnings ratio in the 2018 fiscal year is only 12 times. Some investors with high requirements may still think that they are still not cheap enough. However, judging from the past dividends and growth records of the company, I believe that most of the players are long-term funds, so even if the company is unlucky in 2018, it will meet Vietnam. The sales of large downstream customers are bleak, but considering that the current price has a interest rate of more than 6%, the long-term funds are very rational and do not bring a particularly large golden pit for investors. Another point that may not be considered is that Mutual Textile is Dongli’s first self-owned fabric factory. In the future, Dongli’s resources will be tilted towards each other, and competitiveness will rise sharply. This is a qualitative change. If this is the case, the price-to-earnings ratio is not necessarily limited to an average of 14 times. The company announced on September 29 that the Vietnam plant is about to resume production. About two weeks later, on October 12, there was an 8 million-strong automatic match on the market. It seems that there is already a smart and patience fund that was deployed in the darkest hours before the dawn of the company. After that, I will analyze other supply chain stocks related to Victoria's Secret. Enter [Sina Finance and Economics Unit] Discussion If you like sport SHAOXING LIDONG TRADING CO.,LTD , https://www.lidong-garments.com

Sina Finance App: Live on-line blogger one-on-one guidance

Participate in the Hong Kong stock simulation contest and win the 600,000 prize!

A Hoodie or a Sweatshirt will very well

Wearing it, you don't feel any sense of bondage

You can do whatever you want