After the central bank announced the RRR cut, the funds were not in the same position...

(Original title: After the central bank announced the RRR cut, the funds were not so good...)

After a long period of over-expected easing, in recent days, the sudden and intense tightening of funds has been unprepared.

On the 24th, the overnight repo rate of the interbank market was up to 18%, and the funds within 15% were robbed.

"Now the funds are not tight, they are super tight. In the end, there are still many institutions that have not borrowed money, and many of them have breached the contract." A brokerage official told reporters that the funds in recent days have reached a rare level, most of them. Market participants did not expect that tax payment would have such a significant impact, and the market expects that the RRR will bring a turn for the capital.

The interest rate has smashed the repurchase, and the funds have been "sucked".

However, where the funds are tight, the increase in the interest rate of funds is almost standard, and the rise is fierce. The higher the increase, the tighter the funding.

Since last week, the interest rate of funds has been “suckedâ€, setting a new high.

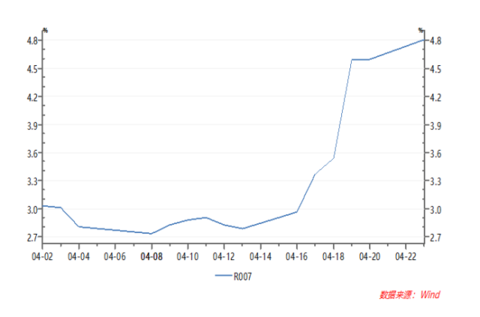

Last Tuesday (April 17), the inter-bank representative 7-day repurchase rate R007 weighted interest rate jumped 40BP, returning to 3% of this "severe line", and then all the way up to 3.54%, 4.60%, 4.80%.

"It's too tight! From last Tuesday, the funds have been tightened sharply, and after a few days it has been extremely tight." Bond market traders said that since last week, the repo market has piled up and piled up, with very little, a small amount. The melt was quickly robbed and the price of funds soared.

It is understood that last week's bank repo rate has been sold to a high of 10%. On Monday, it rose further to 18%.

The currency intermediary daily newspaper said that the funds were still tight on Monday. In the morning, a large amount of 7%-10% of the overnight high price was included in the offer, but the fund-raising party was very few. In the afternoon, there was almost no offer, and all overnight funds within 15% could be quickly sold. The highest turnover was 18%.

"The tension of a few days is extremely depressing, and the market is finally unable to hold back!" Market sources said that some institutions failed to borrow funds on Monday.

The increase in the interest rate of funds indicates that the funds are tight, and the default of repo transactions indicates that the funds are too tight! Historically, only when there is a very tight capital situation, will there be a scene in which the repurchase transaction defaults.

“Monday default is related to a problem with a settlement institution system, but the key is that the funds are too tight, and the market participants are caught off guard.†A person from the asset management agency said that the market was obviously inadequately prepared for the fluctuation of the funds. So nervous.

Since the beginning of this year, the funds have been very loose, and the money market interest rate has dropped a lot. In the week of April 9, the funds were still calm, and there was no shortage of short-term funds in the market. However, since last week, short-term funds have suddenly stopped flowing, resulting in drastic changes in the funds.

Reducing the funding is more stressful than before.

First of all, the amount of tax paid in April is large. The tax clearing income pool is the process of funds flowing from the banking system to the central bank's treasury, and is the process of recycling the base currency.

April is a traditional tax big month. In the past few years, the net increase in fiscal deposits in April was more than 500 billion yuan. Some market participants estimate that the amount of tax withdrawals in the middle of this month may reach the trillion level, and the impact on the short-term supply and demand pattern should not be underestimated. Last week was the peak period of tax payment and storage, which was the period of maximum tax disturbance.

Second, the central bank has returned a lot of funds. Last week, the central bank issued a net investment of 470 billion yuan through reverse repurchase operations. The scale was not small, but it has been net liquidity for four consecutive weeks, with a cumulative net withdrawal of 570 billion yuan. The continuous net withdrawal of the central bank has a cumulative effect, which magnifies the disturbance caused by the large amount of tax paid into the warehouse.

Moreover, before the funds were too loose and optimism rose, some institutions relaxed their liquidity management and the phenomenon of “rolling overnight†reappeared. Under the circumstances that the funds continue to exceed the expected easing, everyone is "rolling overnight". Once the big line does not go out overnight, the funds can not continue, and tension is inevitable.

In addition, while "rolling overnight", there is also "adding leverage." In the first quarter, non-bank institutions bought a lot of bonds and re-added leverage, which reduced the tolerance of fund fluctuations.

It is worth noting that the funding is tight as the central bank announced the RRR cut. On the evening of April 17, the central bank announced that it would reduce the percentage of financial institutions by 1 percentage point in order to replace the medium-term loan facilities. The RRR cut was a strong signal of the total amount of relaxation, but after a few days of announcement, the market funds were very tight.

The reason behind this may be that the tax period disturbance has not been completely eliminated, and the central bank has reduced the open market operation before the implementation of the RRR cut. Since the 20th, the central bank has stopped the net market release.

The moment to wait for the implementation of the RRR

Although the funding is extremely tight, it may not last for too long. The implementation of the RRR cut this week is imminent, and the financial expenditure at the end of the month is extremely strong. The capital fabrics will be “rainy and sunnyâ€.

The central bank said that this time it is a partial reduction of "partial financial institutions" to "replace medium-term lending facilities", but the actual coverage is large, and the RRR is not small. At the same time that it replaces about 900 billion yuan of MWF with a relatively high interest rate. It will also release 400 billion yuan of incremental liquidity.

The essence of this RRR is to replace the short-term and higher-cost funds previously borrowed by the bank from the central bank with long-term, low-cost funds. It is a substantial positive for the funds.

At the same time, at the end of the month, fiscal expenditure will increase, and liquidity will be increased. The impact of fiscal revenue and expenditure on liquidity will also change positively. Therefore, this week's liquidity easing is still a high probability event.

However, this time the funds are tight and I am reminded of everyone. There is room for relaxation in monetary policy. Funds will be better than 2017, but they cannot be expected too high. De-leverage and steady growth should be grasped by both hands, not to mention the various tests of narrowing the spread between China and the United States and inflationary pressures. The currency will not be loose, and the interest rate of funds will not fall too much.

When the re-launching of the leverage has just occurred, it is not necessarily a good thing to have a tight face.

In addition, the current exchange repo rate has risen a lot, although it is unfavorable to the stock market, it provides opportunities for risk-free returns. Participating in exchange repo transactions, low threshold, good security, short-term gains are also good. On the 23rd, the exchange's overnight repo rate rose to a maximum of 10%. However, considering the implementation of the RRR cut, "get on the bus, get it early!"

On-the-spot repo rate on the Shanghai Stock Exchange on April 23

This article Source: China Securities News · Zhongzheng Wang Author: Zhang Qin Feng Editor: Zhong Qiming _NF5619

The shape of the Glasses Frames designed not to hinder the pilot from wearing an oxygen mask became widely known after the US military fought around the world in World War II.

â— BELIEYE's handsome aviator glasses frames show a heroic figure, the integration of Square Glasses Frames lines highlights the chic style of a gentleman, and the classic double-beam design always radiates fashionable charm.

â— The aviator eyeglasses frames can make feminine-style attire three-dimensional at once, and the frame itself has a rigid beauty, which just caters to the new interest in the current fashion industry-following the genderless style.

â— Aviator eyewear frames characteristic of it is that it has a retro undertone, which is not surprising. Today's fashion industry is all about 1970s style, from the feet to the face.

Aviator Glasses Frames,Aviator Prescription Glasses Frames,Transparent Glasses Frames,Aviator Optical Frames,Aviator Eyeglasses Frames,Aviator Eyewear Frames

Belieye (Jiangsu) Co.,LTD , https://www.belieyeglasses.com